You must file an 83(b) election within 30 days of when you are granted the restricted company stock. The grant date is usually the date the board approves the grant, even if you don’t receive the paperwork right away. Taking advantage of your company stock option plan can help you build wealth.

What qualifies for 83b election?

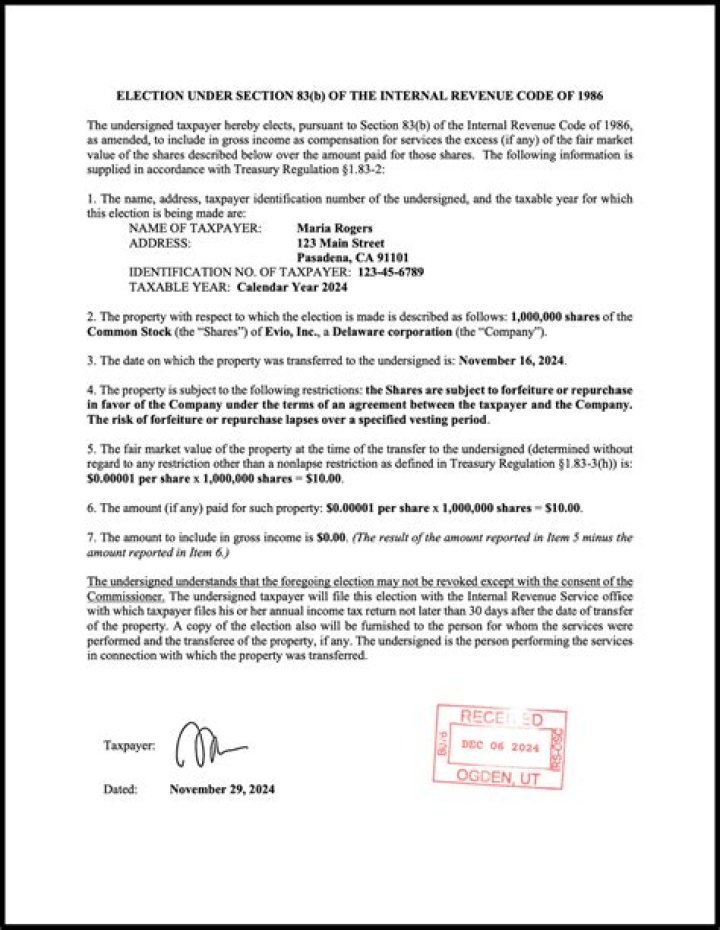

The 83(b) election is a provision under the Internal Revenue Code (IRC) that gives an employee, or startup founder, the option to pay taxes on the total fair market value of restricted stock at the time of granting.

When does 83 ( b ) not apply to vested shares?

Section 83 (b) elections do not apply to vested shares; the election only applies to stock that is not yet vested. Thus, if you receive options that are not early exercisable (meaning you have to wait until they vest to exercise), an 83 (b) election would not apply.

When does the vesting date of Section 83 govern?

A: As background, when property is transferred in connection with the performance of services, Section 83 governs the timing and amount of compensation income taxable to the service provider. The general rule is that the vesting date governs both the timing and amount of taxable income.

What does section 83 ( b ) of the tax code mean?

Section 83 (b) grants any person who performs services in exchange for property the option to include the value of the entire stock, vested and unvested, in their gross income in the initial year of receipt. Essentially, employees have the option to include the stock compensation either at the grant date or as the stock vests. 3.

Do you have to pay taxes on restricted stock when it vests?

This section covers one of the most important and complex decisions you may need to make regarding stock awards and stock options: paying taxes early with an 83 (b) election. Generally, restricted stock is taxed as ordinary income when it vests.