The main difference between accrual and cash basis accounting lies in the timing of when revenue and expenses are recognized. The cash method is a more immediate recognition of revenue and expenses, while the accrual method focuses on anticipated revenue and expenses.

Why is accrual basis preferred?

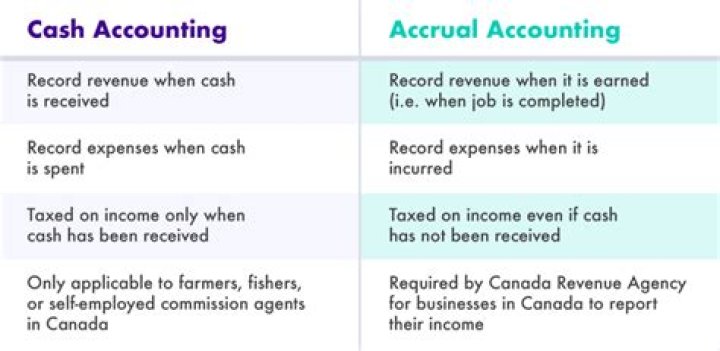

GAAP prefers the accrual accounting method because it records sales at the time they occur, which provides a clearer insight into a company’s performance and actual sales trends as opposed to just when payment is received.

How are cash and accrual accounting systems different?

There are two accounting systems, based on which the transactions are recognised, namely cash system of accounting and accrual system of accounting. The basic difference between the two approaches to bookkeeping of an entity is in timing, i.e. in cash accounting, the recording is done when there is an inflow or outflow of cash.

What are the drawbacks of accrual accounting?

Besides this, one of the major drawbacks of accrual accounting is that the company has to pay tax on the income which is not yet received. The accounting system in which the income or expense is recognised when an exchange of consideration is actually done is known as Cash Accounting.

What’s the difference between cash and modified accrual accounting?

However, the critical difference between the two ways is that the accrual system recognizes the profits earlier, as soon as the transaction takes place. The modified accrual accounting system attempts to incorporate both the cash and accrual system of accounting.

What’s the difference between accruals and receivables in accounting?

In accounting, accruals in a broad perspective fall under either revenues (receivables) or expenses (payables). Accrued revenues are either income or assets (including non-cash assets) that are yet to be received. In this case, a company may offer services or deliver goods, but does so in debt.