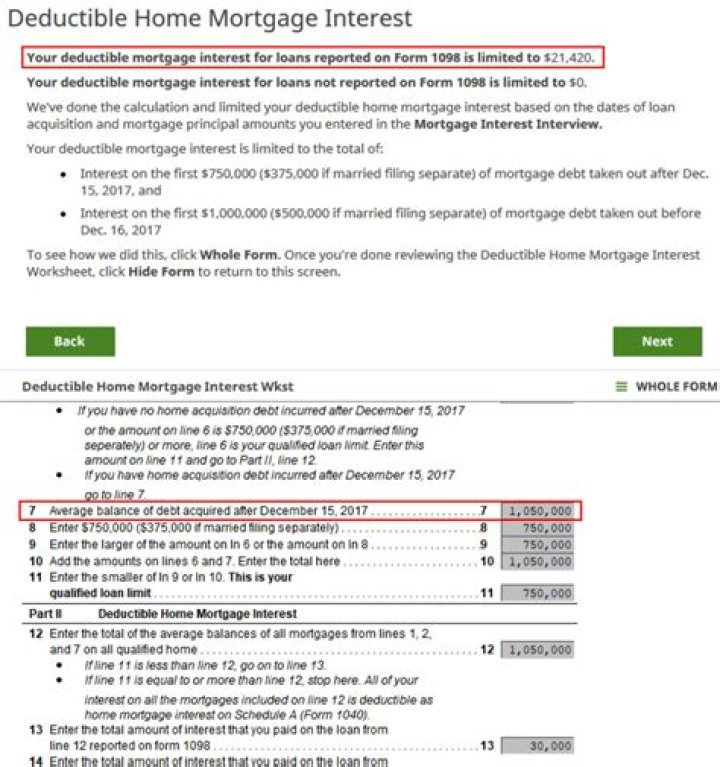

Deductible mortgage interest is any interest you pay on a loan secured by a main home or second home that was used to buy, build, or substantially improve your home. For tax years prior to 2018, the maximum amount of debt eligible for the deduction was $1 million.

Can you deduct mortgage amortization?

You can deduct amortization expenses from your taxable business income, thus reducing your overall tax liability. This can ultimately lower your year-end tax bill. You can spread out amortized deductions over time instead of taking an upfront write-off on the purchase.

Is mortgage principal deductible?

The principal is the total amount you borrow from the lender. It’s not deductible. The portion of your house payment that goes toward the principal is generally smaller during the first years of the mortgage term but increases as the term progresses.

Is any part of a mortgage tax deductible?

Taxpayers can deduct the interest paid on first and second mortgages up to $1,000,000 in mortgage debt (the limit is $500,000 if married and filing separately). Any interest paid on first or second mortgages over this amount is not tax deductible. The marginal Federal tax rate you expect to pay.

Can you deduct mortgage interest on a 1040?

When preparing a decedent’s final income tax Form 1040, or an estate or trust’s Form 1041, you may deduct certain types of interest and taxes. Interest paid on mortgages and stock margin accounts may be deducted, as can real estate tax and state and local income tax. What types of interest can be deducted.

Can you deduct estate tax on Form 1041?

But wait! This rule has an exception. If you elect to pay the estate tax under Section 6166 (that’s an election to spread out the payment of the estate taxes owed over a ten-year period), you get to deduct that interest on Form 1041, even though it’s interest on an unpaid tax bill.

How are depreciation and amortization deductible on Form 1041?

Depreciation, Depletion, and Amortization are all fully deductible (on a pro-rata basis) on Form 1041. Some assets, like homes, appreciate (meaning they increase in value) over time. But some assets decrease in value over time. This is called “depreciation.” A typical example is an automobile.

How are mortgage points considered to be tax deductible?

Origination fees or points paid on a purchase. The IRS considers “mortgage points” to be charges paid to take out a mortgage. They may include origination fees or discount points, and represent a percentage of your loan amount. To be tax-deductible in the same year they are paid, you have to meet the following four conditions.