Rs 2 lakhs

However, the overall loss from house property that can be claimed for a year is restricted to Rs 2 lakhs. As regards 80C deduction, the principal portion of home loan repaid in respect of both houses can be claimed, however within the overall cap of Rs 1.5 lakhs for each financial year.

How long can trading losses be carried forward?

You can carry the loss forward against profits of the same trade in a future year. Claim within four years from the end of the loss making tax year. The cash basis restricts how you can utilise trading losses.

How many years can you take losses?

The IRS will only allow you to claim losses on your business for three out of five tax years. If you don’t show that your business is starting to make a profit, then the IRS can prohibit you from claiming your business losses on your taxes.

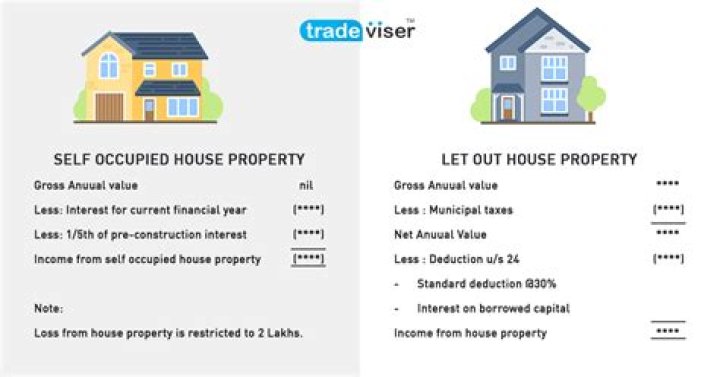

How will you treat the loss from house property?

During a specific assessment year, losses arising out of house property will be allowed to be offset against income from other sources. This loss can be adjusted against income shown under other heads i,e Salary, Business or Profession, Capital Gains or other sources as per the IT act.

How will u set off loss from house property?

The total loss from house property can be adjusted with any other sources of income such as salary etc. The limit for this, however, is at Rs 2 lakh. In case you are not able to set-off the interest of Rs 2 lakh against any of income header, such surplus interest can be carried forward for eight assessment years.

What happens when you sell your home for a loss?

Since capital losses from the sale of a primary residence can’t be used to offset other capital gains or carried forward into future years, the loss provides no tax benefit. The couple benefited from the hot real estate market in their area and sold their home for $1.5 million, resulting in a $900,000 gain after living in the house for five years.

Can you write off home losses on a personal residence sale?

Most people will tell you that you can’t write off home losses on a personal residence sale, but that’s not entirely the case. As with many tax issues, there are loopholes.

How does the IRS calculate a loss on a home?

The IRS uses a home’s value at the point of conversion as the basis for determining a gain or loss. The starting point is either the property’s adjusted basis at the time of conversion or its fair market value at the time of conversion, whichever is less. 3

How many years have you owned your home?

You’ve used the home as your primary residence for two out of the past five years (use test). You’ve owned the home for two out of the past five years (ownership test). You did not use the home sale exclusion in the past two years.