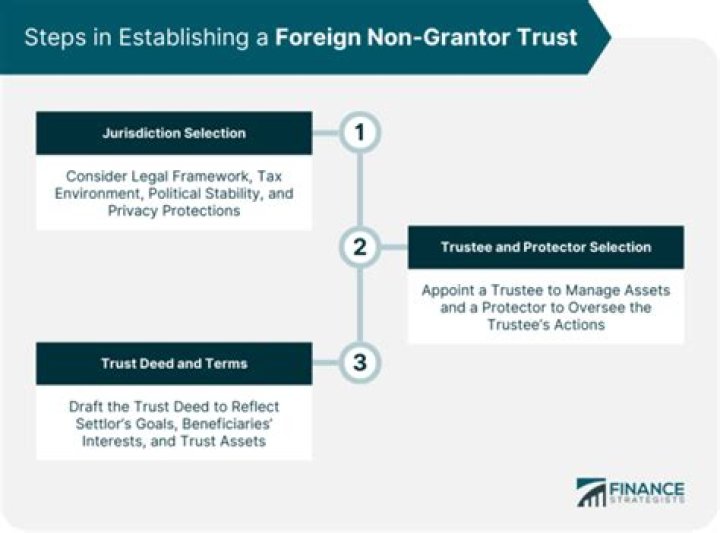

Foreign nongrantor trusts: All foreign trusts that are not grantor trusts are considered nongrantor trusts for U.S. purposes. For U.S. income tax purposes, foreign nongrantor trusts are not generally subject to U.S. tax, unless the trust earns U.S. source or effectively connected income.

Does foreign pension affect Social Security?

Windfall Elimination Provision and Foreign Pensions Your foreign pension will not cause WEP to apply to your U.S. Social Security benefit.

Can a Non-Grantor Trust become a grantor trust?

The conversion from a non-grantor trust to a grantor trust is a taxable transfer of property held by Trust to Grantor as settlor; The conversion from a non-grantor trust to a grantor trust is an act of self-dealing that would result in a tax; and.

When does a pension plan become a foreign grantor trust?

When a pension plan constitutes a foreign grantor trust, there may be a filing requirement to report contributions to, and distributions from, the foreign grantor trust on IRS Forms 3520 and 3520-A. The employee (beneficiary) must report the annual income earned in the plan on his or her U.S. income tax return.

Who is the beneficiary of a foreign pension?

These types of trusts are an employees’ trust in the code. The IRS considers the employer to be the owner of such trusts, rather than the U.S. beneficiary. A non-exempt employees’ trust is the classification that most foreign pensions typically qualify for.

Do you have to report a foreign grantor trust?

When a pension plan constitutes a foreign grantor trust, there may be a filing requirement to report contributions to, and distributions from, the foreign grantor trust on IRS Forms 3520 and 3520-A.

Can a foreign trust be taxed in the US?

U.S. tax is limited generally to U.S. sourced investment income and income effectively connected with a U.S. trade or business will be subject to U.S. income or withholding tax. If a U.S. grantor establishes a foreign trust for the benefit of U.S. beneficiaries, it is treated as a grantor trust. I.R.C. §679.