Bonus depreciation is a valuable tax-saving tool for businesses. It allows your business to take an immediate first-year deduction on the purchase of eligible business property, in addition to other depreciation.

What can you take bonus depreciation on?

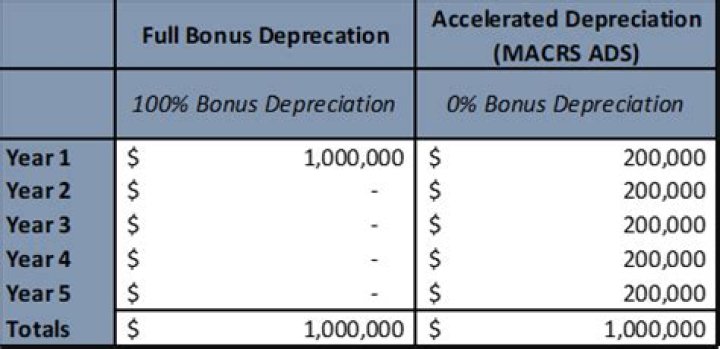

How bonus depreciation works

- Property that has a useful life of 20 years or less. This includes vehicles, equipment, furniture and fixtures, and machinery.

- Qualified improvement property.

- Computer software.

- Some listed property.

- Costs of qualified film or television productions and qualified live theatrical productions.

When was the 100 percent bonus depreciation created?

The 100% additional first year depreciation deduction was created in 2017 by the Tax Cuts and Jobs Act and generally applies to depreciable business assets with a recovery period of 20 years or less and certain other property.

What can I deduct on my taxes with bonus depreciation?

With bonus depreciation, you can deduct the cost of both your staplers and heavy machinery in the year purchased and put to work. The processes to deduct both expenses vary, but the bottom-line impact is the same. The Tax Cuts and Jobs Act of 2017 (TCJA) increased the deductible amount from 50% to 100% of an eligible asset’s cost.

When to use transition rule for bonus depreciation?

A transition rule provides that for a taxpayer’s first taxable year ending after Sept. 27, 2017, the taxpayer may elect to apply a 50 percent allowance instead of the 100 percent allowance. Taxpayers can still elect not to claim bonus depreciation for any class of property placed in service during the tax year.

When does bonus depreciation end for new homes?

80% for property placed in service after December 31, 2022 and before January 1, 2024. 60% for property placed in service after December 31, 2023 and before January 1, 2025. 40% for property placed in service after December 31, 2024 and before January1, 2026. 20% for property placed in service after December 31, 2025 and before January 1, 2027.