Any trade or business involving the performance of services in the field of law, consulting and accounting, amongst other services, is considered a specified service trades or business (“SSTB”), and therefore does not qualify for Section 199A deduction unless the individual taxpayer of an SSTB has a taxable income …

Do partnerships get 199A?

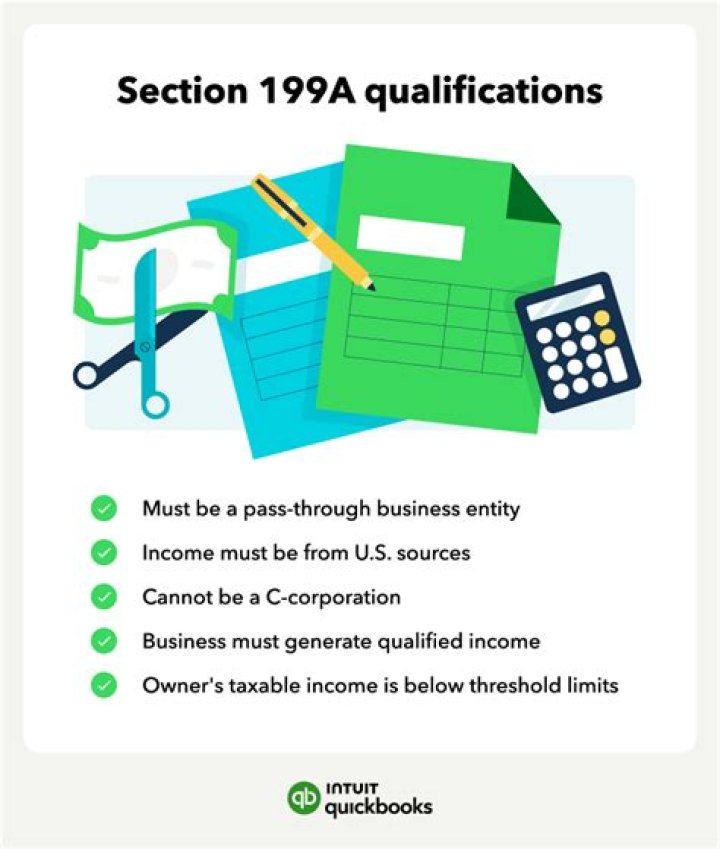

Section 199A of the Internal Revenue Code provides many owners of sole proprietorships, partnerships, S corporations and some trusts and estates, a deduction of income from a qualified trade or business.

Does Section 199A apply to trusts?

Section 199A does apply to non-grantor trusts and its beneficiaries. The taxable income threshold amounts follow that of single individuals.

Can a lawyer get a Qbi deduction?

Qualified business income (QBI) is defined as the owner’s share of pass-through entity net income usually reported on the owner’s Schedule K-1. Therefore, law firms are not included in the definition of a “qualified business” and generally do not qualify for the special 20% deduction.

Are lawyers Sstbs?

Defined as an SSTB: The performance of services by individuals such as lawyers, paralegals, legal arbitrators, mediators and similar professionals performing services in their capacity as such. Not considered an SSTB: The provision of services that do not require skills unique to the field of law.

Is the 199A deduction available to law firms?

Service professionals have specific limitations under this section. Law firms, solo and otherwise, should revisit tax status and entity structure early in 2018 to determine whether restructuring is in order to benefit from the new tax law. The 199A deduction is available to individual taxpayers and trusts who own pass-through trades or businesses.

How are partnership interests affected by section 199A?

Examining Section 199A in the partnership context, owners of partnership interests will now need to consider how the allocation methods of the partnership will ultimately characterize the income allocated to that individual for purposes of the 199A deduction.

What is qualified business income under section 199A?

Section 199A(c)(1) defines qualified business income as the net amount of qualified items of income, gain, deduction, and loss with respect to any qualified trade or business of the taxpayer.

How are guaranteed payments treated under section 199A?

This payment would not be contingent upon the partnership making a certain level of income and would be considered a guaranteed payment. For income tax purposes, this type of payment is treated as if it was made to an individual who was not a partner of the partnership. It would not qualify for the Section 199A deduction.