However, a partner’s “tax basis capital” account can be negative if a partnership allocates tax losses or deductions or makes distributions to the partner in excess of the partner’s tax basis equity in the partnership, or when a partner contributes property subject to debt in excess of its adjusted tax basis to the …

What happens if you have a negative capital account?

A negative capital account balance indicates a predominant money flow outbound from a country to other countries. The implication of a negative capital account balance is that ownership of assets in foreign countries is increasing. These decrease the capital account balance and add to the current account balance.

Can a limited partner have a negative capital account?

A partner’s capital account cannot begin with a negative balance. However, a partner can have a negative capital account after accounting for the partner’s distributive share of losses and/or distributions. A partner’s outside basis should never have a negative balance.

What does negative balance of payments mean?

A negative balance indicates that your bill was overpaid and that you may be eligible for a refund. You may only receive your refund after the semester starts and your anticipated credits are disbursed to your student account.

Can a LLC have a negative capital account?

Partners and members of an LLC taxed as a partnership will often have negative or deficit capital account balances at the end of a taxable year. A negative capital account balance is permissible if supported by proper allocation of partnership debt (or an obligation to restore a deficit).

Can a partner’s tax basis capital account be negative?

A partner’s tax basis capital account can be negative when its outside basis is zero or positive because outside basis is increased by the partner’s share of partnership liabilities under § 752 and the partner’s tax basis capital account is not. A partner’s tax basis capital account can be negative if a partnership

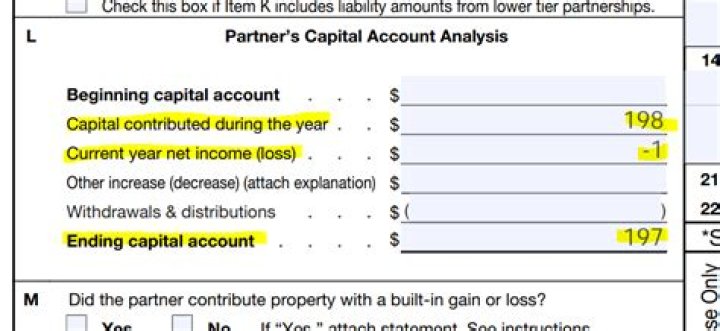

Can you have a negative capital account on k 1?

A partner’s tax basis capital account can be negative if a partnership allocates tax losses or deductions or make distributions to the partner in excess of the partner’s tax basis equity in the partnership, or when a partner contributes property subject to debt in excess of its adjusted tax basis to a partnership. Click to see full answer.

When does a capital account have to be negative?

Under certain conditions, the IRS allows a capital account to be negative at the end of each fiscal year. This can occur when the cumulative distributed cash and allocated losses exceed a partner’s capital contributions plus allocated income to date.