A primary residence is not an investment property and thus has different tax outcomes. Primary residence homeowners can take advantage of certain tax benefits when selling their home. This benefit is called section 121 primary residence tax exclusion.

Is the sale of a primary residence a loss or gain?

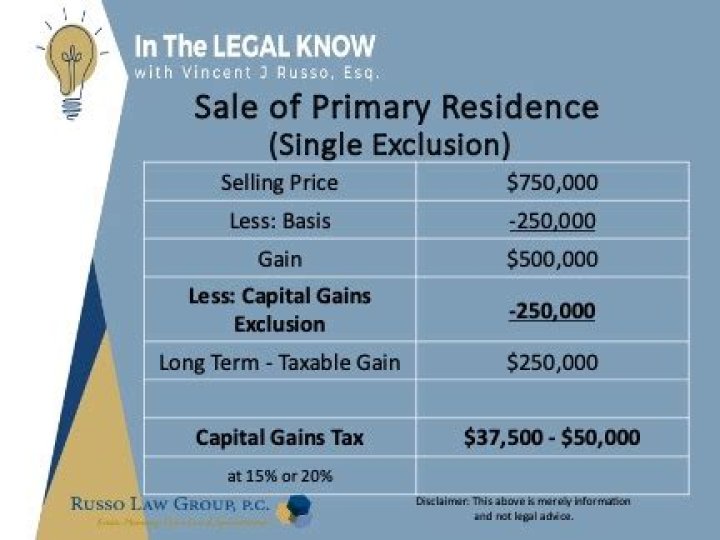

The sales price minus the basis (plus sales cost) equals the gain or loss. A larger basis will result in a smaller gain and thus less in taxes. If you sell your home below the basis, you’ll have a loss. A loss on a primary residence is not deductible. Even if you don’t owe any taxes, it’s best to report it on your tax return.

Is there an exclusion on the sale of a primary residence?

The exclusion applies to federal taxes only. State taxes still apply but may be reduced if the state has a credit or other favorable tax reductions on the sale of a primary residence. From the above example, the $63,000 is an allowed exclusion. Taking another scenario, the allowed exclusion on a $300,000 gain for a single filer is $250,000.

Do you have to pay capital gains on primary residence?

Primary Residence Capital Gains Tax When selling a home for a gain, you may owe taxes. If you’ve lived in the home for more than a year, you’ll pay long-term capital gains taxes.

There are tax benefits for selling a primary residence that won’t be available on a long-term rental property. When selling your converted rental property, you lose the home sale exclusion. In 2015, the first $250,000 for single,…

How are capital gains taxed when selling a rental property?

Selling rental properties can earn investors immense profits, but may result in significant capital gains tax burdens. There are various methods of reducing capital gains tax, including tax-loss harvesting, using Section 1031 of the tax code, and converting your rental property into your primary place of residence.

Can a primary residence be a rental property?

If getting your equity out of the property isn’t a must, you may also consider using the house to generate income as a rental property. This is the first of two articles about converting a principal residence to a residential income property.

How is the tax basis of a primary residence calculated?

There is a formula for computing the tax basis of a personal residence converted to rental property. In general, the adjusted tax basis of a primary residence is the purchase price of the home plus amounts spent for capital improvements that have added value to the property, prolonged its life, or adapted it for a new use.